Elite Homes in India: A Future-Ready Investment for NRIs

For long-term, risk-free wealth creation in India, the Public Provident Fund (PPF) remains a top choice. Whether you're...

Read More

by

Ashiana Housing Ltd /

/

Reading Time: 3 minutes/

With many positive changes, 2019 looks like a good year for the housing sector as buyers can finally acquire their dream home. Property prices, currency and inflation are stagnant, interest rates are lower and numerous tax incentives and subsidies like PMAY are giving the real estate market a much needed boost with a new wave of affordability. The demand for home loans is expected to go up from the present 28% to 40% by 2025. Budget 2019 has proposed to hike the deduction which is claimed for interest paid on housing loans by Rs.1.5 lakh to Rs.3.5 lakh per annum for homes valued up to Rs.45 lakh, which is available on loans taken up to 31 March 2020. With this deduction, the total benefit becomes Rs.7 lakh for a loan tenure of 15 years. This move will further boost the demand for affordable homes.

Housing is the 4th largest contributor to the country’s GDP and has the potential to drive domestic growth. The housing

demand is at an all time high in 2019 because of rapid urbanisation with demographic focus on nuclear families, lower penetration of mortgage and 65% of the population being below the age of 35. Interest rates will mostly be stable but banks are now switching to an external benchmark to determine rates which may create volatility in the short run but will be beneficial in the long run for home loan borrowers.

Those who have taken home loans from NBFCs and HF

Cs are safe from any rate hikes because as per RBI’s mandate, only banks are required to link their retail loans to external benchmarks and not other financial institutions. Due to the recent cut in the repo rate by RBI, all major banks like SBI and ICICI Bank has cut interest rates on deposits plus home loans by 0.1% which has come into effect from 1 July 2019. The National Housing Bank has also instructed banks to not charge prepayment penalty on home loans and SBI has waived it with other banks expected to follow suit.

The Indian home loan market is fairly commoditised unlike the one in developed nations. Apart from interest rates, few factors determine whether one would get a loan or not like loan amount, tenure, credit worthiness etc. There is scope for newer financial products like an overdraft facility which can offered instead of a term loan as a financing option for a house.

Home Loan Interest Table (2019)

| Financial Institution | Home Loan Rates |

|---|---|

| SBI (State Bank of India) | 8.55% – 9.05% |

| HDFC Ltd | 8.70% – 9.15% |

| ICICI Bank | 9.05% – 9.25% |

| Axis Bank | 8.80% – 9.05% |

| IDBI Bank | 8.85% |

| Bank of Baroda | 8.70% |

| Union Bank | 8.60% – 8.65% |

| Dena Bank | 8.55% – 8.85% |

| PNB Home Loan | 8.60% – 8.70% |

Source: paisabazaar.com

Home loan interest rates vary from lender to lender. Currently, SBI offers the lowest home loan rate starting at 8.4%. Base Rate in a loan is the minimum rate of interest set by the RBI that is levied on the borrower. Sometimes financial institutions charge a lower rate of interest to attract more borrowers, which is detrimental to the transparency of the credit market. Hence, RBI sets this minimum rate of interest rate to maintain clarity and consistency in credit market and restrict any malpractices. Base rate and home loans have a directly proportional relationship.

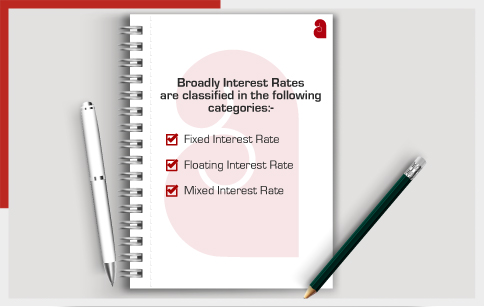

Broadly interest rates are classified in the following categories:

Fixed Interest Rate is quite self explanatory; interest rate which stays fixed all throughout the tenure of the loan is called fixed interest rate.

Floating Interest Rate is also called a variable rate of interest and is subject to the latest lending rates of the bank. Unlike the fixed rate of interest, floating interest rates may change during the loan tenure. The rate is dependent on various factors such as RBI’s monetary policies, revised MCLR (Marginal Cost of funds based Lending rate) or other lending rates, etc.

Mixed Interest Rate stays fixed for a predetermined period for the house loan and after that become a floating rate of interest.

Banks and HFCs (Housing Finance Companies) charge a higher rate of interest on fixed and mixed rate home loans so that they can compensate for any future loss in interest income which may arise out of interest rate volatility. For example, Union Bank of India’s interest rate starts from 8.7% p.a. for floating rate home loans, whereas the interest rate for their mixed-rate (fixed for up to 5 years) home loans start from 11.40% p.a. Onwards.

Providing loans and setting interest rates are completely the prerogative of the lending financial institution. There is no set formula to avail home loan at a low rate but a few key practices can help you get the best rates available:

Opt for a joint home loan with your spouse and the wife should be named the primary applicant. Home loans to women are provided on an interest rate which is less than 0.5% of the general rate.

Opt for a home loan balance transfer in case the current financial institution is charging a high rate of interest and switch to one which provides a lower rate of interest. Competition is quite tough and banks don’t want to lose good customers who make timely payments and have a good credit history.

Housing Loan Interest Rates at NBFCs in India July 2019

| NBFCs | Interest rates |

|---|---|

| Bajaj Finance/Finserv | 8.85% – 11.15% |

| DHFL | 9.05% – 9.95% |

| Fullerton India | 8.50% – 17% |

| HDFC Ltd | 8.55% – 9.55% |

| Indiabulls HFL | 8.80% – 11.05% |

| LIC Housing Finance Ltd | 8.60%-9.15% |

| PNB Housing Finance Ltd | 9.05% – 12.00% |

| Reliance Home Finance | 8.75% – 14.00% |

| Tata Capital | 8.90% – 9.35% |

| Piramal Housing Finance | 9% – 9.10% |

Source: wishfin.com

The Top 10 Home Loan Providers in India are:

1. State Bank of India (SBI)

2. ICICI Bank

3. HDFC Bank/HDFC Ltd.

4. Axis Bank

5. Dewan Housing Finance Ltd. (DHFL)

6. Indiabulls Home Finance

7. LIC Housing Finance

8. PNB Housing Finance Ltd.

9. Bank of Baroda (BOB)

10. Aditya Birla Housing Finance Limited

“A home isn’t a place but a feeling; feeling of safety, security, ownership and familiarity. Renting is a good short term option but people prefer owning homes because homes increase in value, build equity and provide a nest for the future. Keeping in mind the current trend in real estate, the Govt. has thus brought in positive reforms which will assist citizens in owning a house irrespective of their economic background. More demand will promote upward growth in the housing sector leading to a positive trickle-down effect in other sectors also.”

Related Blog:-

How to Pick Winning Investments that Offer High Returns at Low Risks?